May 2022 Macro Update

May 2022 Macro Update

Cautiously Optimistic but Risks Remain

I hope everyone is doing well! Welcome to all my new subscribers!

Nothing that I say below is investment advice and the views below are subject to change at any time. These views are my views and not of any firm that I am associated with. Please read the disclosure at the end of this article for more information. Subscribe below!

It sure has been a volatile Q1 and I think volatility will remain with us for the coming quarters. Are we headed for a crash? I don’t think so. As I’m writing this, the U.S. stock market has lost $7 trillion in value so far this year. I personally believe this will be a rocky period, but I don’t think this will be a repeat of the global financial crisis. There are a couple of things I am watching that are becoming concerning only if the trend continues to get materially worse from here. The global economy is highly connected so any further disruptions could cause further damage to risk assets. I want to lay the groundwork because it is critical to see the bull and bear case to make the best judgements based on the data that we all are provided.

First, it all comes down to cash - corporations are stronger than ever. The total liquid assets of US non-financial corporations have amassed $7.1 trillion compared to the $2 trillion that it was at the end of Q2 in 2009. The cash needs go somewhere so I think we will see a massive M&A wave and corporations will continue to buy back their own stock. Not only are corporations stronger, but also private equity and venture capital firms are sitting on more than $2 trillion dollars, which is the largest cash pile in history. Lastly, investors amassed $4.7 trillion in money market funds at the end of 2021, which is close to a record according to data from Goldman Sachs. To conclude, over $13 trillion dollars is sitting in cash at this time ready to be deployed.

Secondly, one of the biggest talking points is inflation. If we look at a recent survey by BofA Global Research, investors are at the highest overweight to commodities in the history of the survey. This is indicative that commodities are overdone in the short-term. When we look back in a few quarters, I believe some commodity prices will moderate off stretched prices while others may stay elevated due to global factors.

One area that we’re seeing some positive developments is in the Manheim Used Vehicle Value Index. Prices have skyrocketed after the pandemic. Lately, if we look at the chart below, you can see some relief. I think we will see a meaningful correction in the coming quarters as consumer spending slows due to higher inflation pressures across the board.

Another area that has some positive development is in the lumber market. Lumber prices in the beginning of the year surged north of $1,300 per board feet and tripled from lows set last summer.

This added roughly $18,600 to the cost of a new single-family home according to NAHB standard estimates. Since the highs set back in March, prices are down 40% from the highs giving some relief to builders and homeowners looking to remodel homes. As we can see in the chart below, the great remodel boom is here and there are millions of homes that are 30 to 40+ years old that may also need updating. I believe the housing market will remain very strong over the next 10 years but could see a slowdown in the near-term due to rising mortgage rates and higher prices. 1

Number of homes in the United States as October 2021, by age (in millions)

We are currently experiencing a housing shortage in the United States that I think will last a few years. I have seen estimates that we are short 3-5 million homes in the United States. Thankfully, new home construction is at at the highest levels in over a decade to meet the significant demand of the Millennial generation.

One area that I am particularly concerned about is food inflation. In the recent CPI report, food at home index was up 10.8% over the last 12 months, which is the largest 12 month increase since November of 1980. While food shortages are not a dire level, countries are starting to move towards a “protectionist” environment. Over the weekend, India said it would be banning wheat exports to curb prices in their country as inflationary pressures are hitting consumers in India.

Another reason why I believe food prices will remain higher than normal is the parabolic increase in fertilizer prices, which is something we highlighted a few months ago. The war between Russia and Ukraine is not helping the issue as the two countries together export 28% of the fertilizers made from nitrogen, phosphorus, and potassium according to Morgan Stanley.

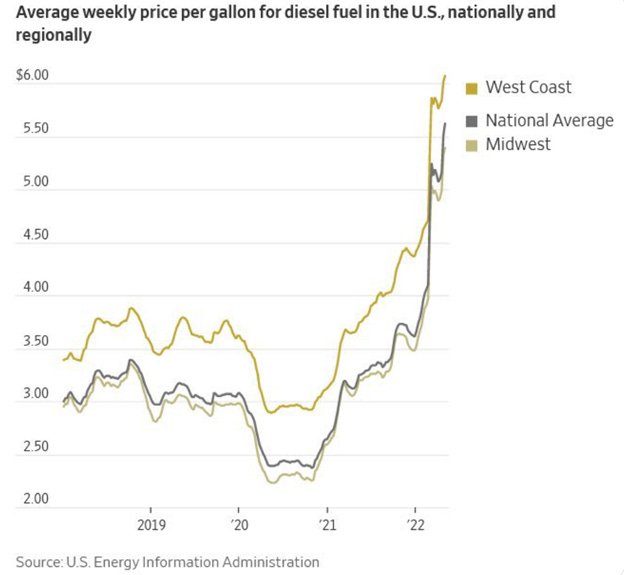

Another area of concern is energy costs. In the recent CPI release, the energy index rose 30.3% over the last year. The war is without a doubt a contributing factor, but production levels are at 11.9 million barrels per day. Unfortunately, crude production is still down 1.2 million barrels per day prior to the pandemic. There is a lag when companies can add meaningful amount of production and when prices are high. I expect production levels to gradually increase in the coming months, but I’m not expecting that will have material impact in the near term. The biggest risk to prices is military action by Russia towards a NATO country, which would lead to an oil price shock pushing prices north of $150-$200 a barrel. The best case scenario would be a ceasefire, which would lead to a major correction in oil and natural gas prices. The chart below depicts the massive increase in diesel fuel prices over the last 12 months.

Also, Germany recently announced they will be banning oil imports of Russian oil by year end regardless of what the EU decides with the next round of sanctions. Recent research done by Goldman Sachs estimated that a total embargo of Russian gas could see Eurozone’s GDP contract by 2.2%.2

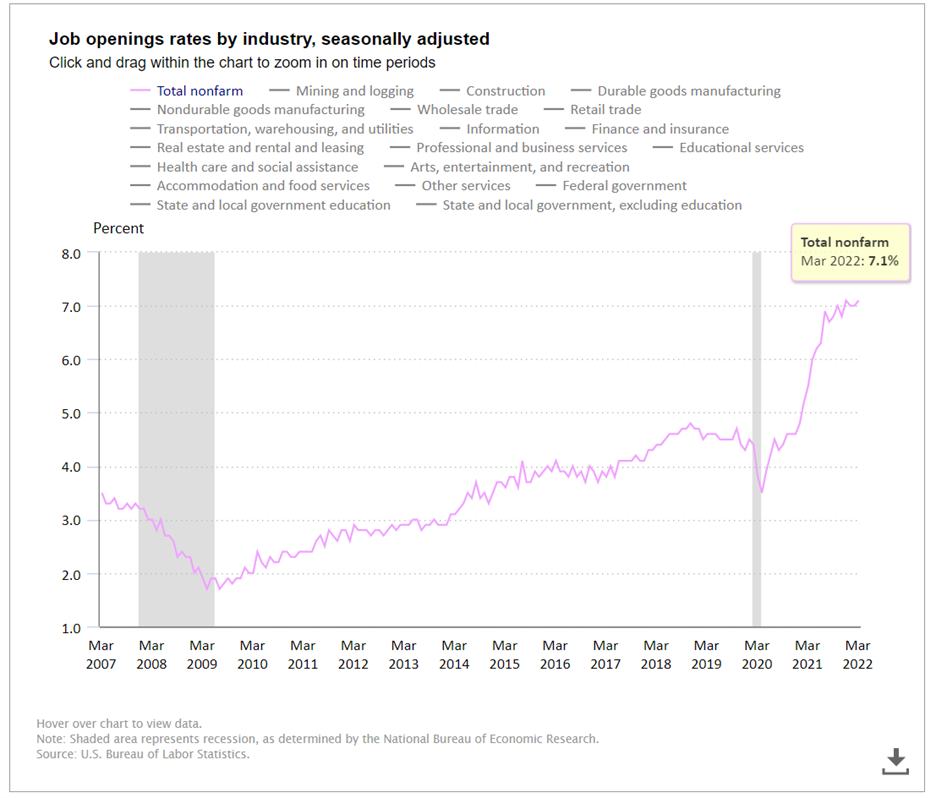

Shortages in labor continue to grow and look to be getting worse. This chart below shows just how strong the economy is right now, but it is a cause for concern that shortages in certain industries may last longer than expected as lack of workers may cause delays.

Global debt is at historic highs due to the pandemic. Rising interest rates are cause for concern as the debt load has never been higher. One of my biggest fears is a debt crisis that spreads globally leading to another global financial crisis. This is something to watch for sure. The debt load around the world is so large the Fed knows they can’t move too quickly or something may break, which could lead to a domino effect.

Lastly, I want to focus on the Federal Reserve. There is no doubt that the Fed is behind the curve, and they made a mistake by delaying rate hikes until this year. The Fed is forced to hike rates to slow down the expansion to allow supply chains and for supply/demand to reach somewhat of an equilibrium. Right now, supply chains are recovering from the COVID crisis, and it may take a few quarters to normalize. The absolute key is the speed of the rate increases. If the Fed moves too quickly, I fear it may cause a potential hard landing. If they move too slowly, inflationary pressures may persist causing a global slowdown and making the Fed reverse course to cutting rates and relaunching quantitative easing. I think the new normal rate will sit around 2.5% to 3% on the Fed funds. I think after a few more hikes they will signal they are getting closer to achieving their goal.

Now that the Fed and government are so used to low rates and higher deficit spending, the Fed will most likely be buying bonds and lowering rates sooner than most think. These tools have been so effective since the crisis but are causing major wealth inequality across the United States. Roughly 55% of Americans who own stocks have benefited from the tremendous wealth that has been created over the last decade. However, one has to wonder what will happen to the other half. I think it is going to be hard to stay away from accommodative monetary policy and move towards a tighter policy for a sustained period due to the lack of mediocre growth rates we have experienced since the global financial crisis.

Thanks for reading,

Korey

The publication of this newsletter falls outside of the scope of Korey Bauer’s (“Bauer”) employment with AXS Investments, LLC (“AXS”), and Bauer does not represent AXS in its publication. The views expressed in the newsletter solely represent the opinion of Bauer and do not reflect the views or opinions of AXS. Bauer’s opinions are subject to change and are not intended as a forecast or guarantee of future results, or investment advice. Stated information is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While Bauer believes the information to be accurate and reliable, he does not claim or have responsibility for its completeness, accuracy, or reliability. The newsletter is made available for informational and educational purposes only and is not intended to be a substitute for professional investment advice tailored to your specific circumstances. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Bauer’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. These are Bauer’s views, and no company is responsible.

Exclusion of Liability: To the fullest extent allowed by law, neither AXS Investments, LLC nor Korey Bauer shall be liable for any direct, indirect, or consequential losses, loss of profits, damages, punitive damages or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this newsletter, which is provided as is and without warranties.

https://www.nahb.org/blog/2022/01/latest-wave-of-rising-lumber-prices-adds-more-than-18600-to-the-price-of-a-new-home/#:~:text=Over%20the%20past%20four%20months,to%20build%20the%20average%20home

https://www.politico.eu/article/ban-on-russian-gas-risks-reviving-populism-in-europe/