The Biggest Wealth Transfer in American History is Coming…

The Biggest Wealth Transfer in American History is Coming…

I hope everyone is doing well! First, I would like to thank all the veterans out there who served and sacrificed their lives for our country! Also, thank you to my first handful of subscribers for signing up. Nothing that I say below is investment advice and the views below are subject to change at any time. These views are my views and not of any firm that I am associated with. Please read disclosure at the end of this article for more information. Subscribe below!

Today’s letter is looking at the tidal wave of wealth that is about to be transferred to the next generation over the next 20-25 years. What are the two main drivers of the amount of wealth that has been created in the United States over the last 30-40 years? The stock market and housing!

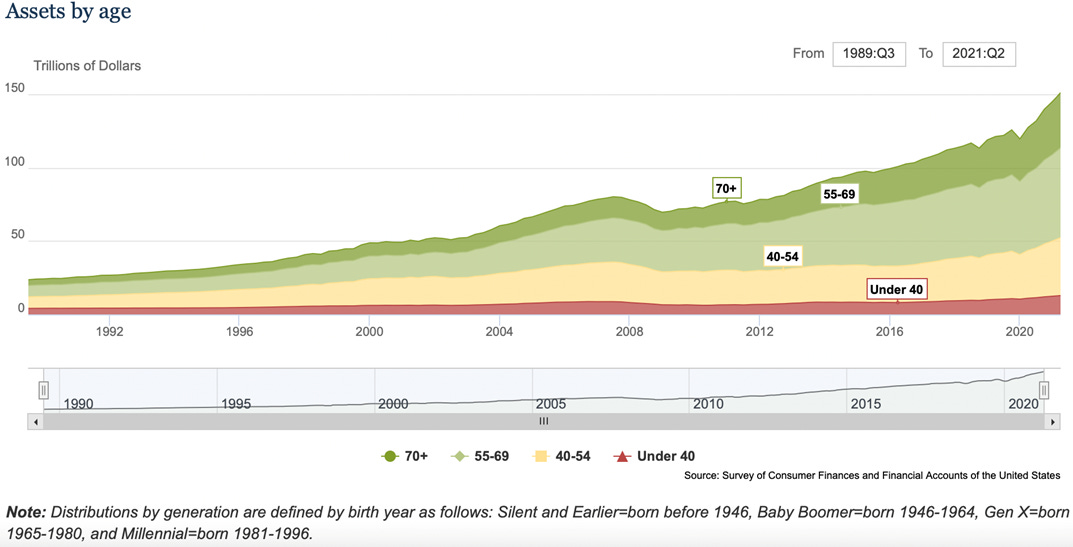

If we look at the chart below, the baby boomer generation controls a major portion of the roughly $151 trillion dollars of total assets held by the American public.

This is one of my favorite charts that shows the assets by generation. The Baby Boomers control $73.66 trillion in assets which nearly is more wealth than the other three generations combined.

Note: Distributions by generation are defined by birth year as follows: Silent and Earlier=born before 1946, Baby Boomer=born 1946-1964, Gen X=born 1965-1980, and Millennial=born 1981-1996.

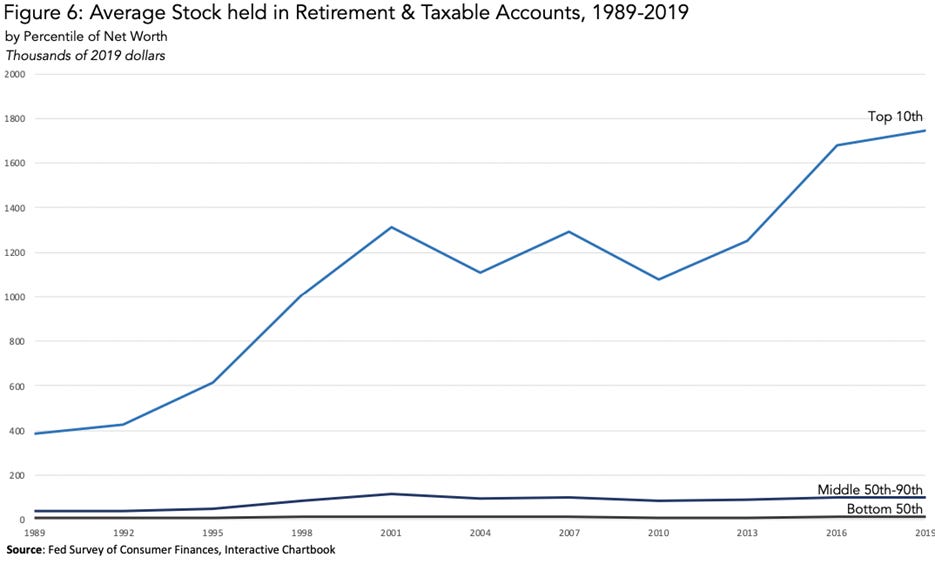

So how many Americans own stocks? Roughly 53% of Americans are invested in the stock market. But if we drill down further, ownership of stocks is mostly being held by people with higher incomes. American families that are in the top 10% of income held roughly 70% of the total value of all stocks in 2019. The chart below depicts the “top 10% of households, on average own $1.7 million of stock, directly and indirectly, while the bottom 50% only own about $11,000”.[1] The wealth gap here is something that needs to be addressed as we need to educate Americans on the power of investing. I understand wealthy families make more money but a small amount of money that is saved over a long period of time can grow. For example, if you save an extra $100 a month and invest it over a 40-year period at a 7% return, that account could be potentially worth $240,000. This is the power of compounding!

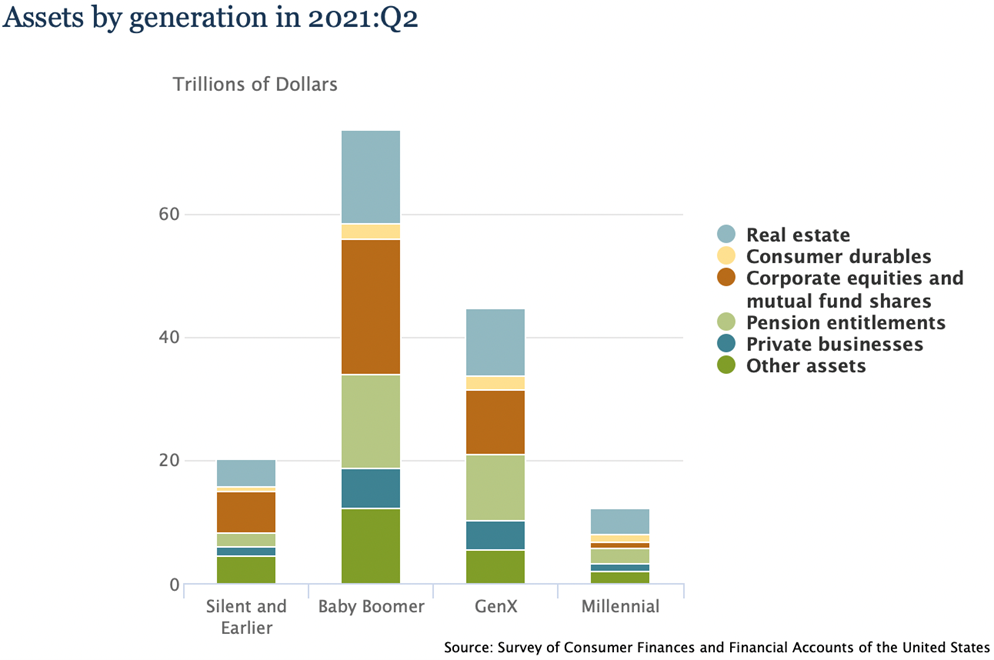

If we look at ownership of equities, investors who are 55 and older own a whopping 72% of the stock market while investors under 44 only own 9.7% of the stock market. Equities now make up $40+ trillion of financial assets of Americans! The under 40 crowd needs to catch up but unfortunately, they continue to rack up debt with roughly 30% of the overall liabilities if we look at the distribution of household wealth in the United States.

Here is another great chart showing the breakdown of corporate stock in retirement accounts. It’s amazing how popular Individual Retirement Accounts (IRAs) became after they were introduced in 1978!

The Baby Boomers, who are the wealthiest generation in American history, are moving towards retirement. Why is the Federal Reserve so hesitant to raise interest rates? Simple. The wealth effect is alive and well and the American public has never been wealthier. Asset prices (stock market) and housing prices are both at record highs in the United States. A drop in the stock market is detrimental to the masses not only for the wealthy but also for people who have saved money in IRAs and defined contribution plans as well. Inflated asset prices have helped many Americans retire and open the door for younger Americans to fill those jobs.

So, the $73 trillion dollar question is how the money will be invested in the future? Will future generations maintain their parents stock portfolios? Or will cryptocurrencies become a threat to the traditional mega cap technology business models causing a major reallocation of financial assets? A big transformation is coming in America in the coming decades, and I can’t wait to see how things play out.

Thanks for reading and please subscribe to receive future updates. Please forward to anyone who you think can benefit from this information.

Cheers,

Korey Bauer

The publication of this newsletter falls outside of the scope of Korey Bauer’s (“Bauer”) employment with AXS Investments, LLC (“AXS”), and Bauer does not represent AXS in its publication. The views expressed in the newsletter solely represent the opinion of Bauer and do not reflect the views or opinions of AXS. Bauer’s opinions are subject to change and are not intended as a forecast or guarantee of future results, or investment advice. Stated information is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While Bauer believes the information to be accurate and reliable, he does not claim or have responsibility for its completeness, accuracy, or reliability. The newsletter is made available for informational and educational purposes only, and is not intended to be a substitute for professional investment advice tailored to your specific circumstances. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Bauer’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. These are Bauer’s views, and no company is responsible.

Exclusion of Liability: To the fullest extent allowed by law, neither AXS Investments, LLC nor Korey Bauer shall be liable for any direct, indirect, or consequential losses, loss of profits, damages, punitive damages or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this newsletter, which is provided as is and without warranties.

Charts/Sources:

https://www.federalreserve.gov

[1] https://www.law.nyu.edu/sites/default/files/Who’s%20Left%20to%20Tax%3F%20US%20Taxation%20of%20Corporations%20and%20Their%20Shareholders-%20Rosenthal%20and%20Burke.pdf