Inflation: Is it all priced in?

Inflation: Is it all priced in?

Thanks for taking the time to read my first newsletter post. I hope to do these as often as I can and would appreciate any feedback. First, nothing that I say below is investment advice and the views below are subject to change at any time. These views are my views and not of any firm that I am associated with. Please read disclosure at the end of this article for more information. Subscribe below!

So, let’s jump right in and talk about the elephant in the room. Inflation. Will it stay here? Is it transitory? Is it already priced in?

CPI:

U.S. CPI (Consumer Price Index) surged at its fastest pace in 13 years as the Labor Department’s Consumer Price Index, which measures a basket of goods, was up 5.3% in August from a year earlier. This is slightly lower than last month’s reading that came in at 5.4%. This is the highest CPI has been since 2008 putting pressure on consumers and companies that are dealing with high shipping costs and rising labor costs. If we look at the recent CPI reading, the majority of the subcomponents that make up the reading are all moving higher which is not a good sign.

After reviewing the inflation readings, we can see certain aspects are starting to show signs of softness. Airline fares were down 9.1% over the last month. Two areas that we don’t think may be priced appropriately at this time are food and energy costs. We will dive deeper into these two sectors below.

Housing:

The national index for rental prices month-over-month has increased 2.1% from August to September. Just how expensive has renting become post COVID? This year, the national median rent growth has increased by 16.4% according to Apartment List. How does that compare with historical trends? Well, from 2017-2019 and from January until September during that same timeframe, rent growth averaged a much more normal pace of 3.4%. One could make the argument that these price increases are temporary as landlords were hit last year during the COVID outbreak. The good news is vacancies ticked up for the first time since last April which could put a near term halt on price increases. Again, we still need to see more data in the coming months to support that this shift has some legs.

While rents are currently surging in the United States all over the country, we think the rate of price increases are starting to cool and should lead to a normalized environment for renters in 2022.

The housing market prices in the United States soared in July, up 19.7%. This was the largest jump in over 30 years according to S&P CoreLogic Case Shiller Index of property values in the U.S. If you look at the chart below, this is the 14th straight month of price gains for property values.

Is there an end in sight for home buyers? I think so. Existing home sales dropped 2.0% on a seasonally adjusted annual rate of 5.88 million units in the month of August (white line in the chart below). Also, if we look at the number of homes that are available on the market today, we have seen a meaningful uptick from 2020 when there was less than 2 months of supply. Now we’re at 2.6 months of inventory (blue line in the chart below).

Source: Bloomberg

Conclusion: I think housing prices will start to normalize at a much slower pace sometime in the next few quarters. I do think demand will continue to outstrip supply in the near term as many new home buyers continue to enter the market. If the Fed does indeed start tightening/tapering, this could lead to some softness in the real estate sector as rates start to climb. Just keep in mind, if you think housing prices are severely overvalued, I will caution that mindset as U.S. housing prices have not kept pace with some other developed nations in the last 20+ years. For example, the Canadian housing market prices are 168% higher than where they were in Q1 2000 relative to the U.S. which was 50% higher at the end of Q4 2020.

(Chart Source: The Economist)

Lumber:/Building Materials

At the beginning of the year lumber prices started at $700 per thousand board feet. By May, prices skyrocketed up to $1700 per thousand board feet causing major headwinds for homebuilders and homeowners looking to remodel. It didn’t last long as prices collapsed over 70% down to $400 which has been a relief for the construction industry. On the other hand, more than 90% of builders are reporting shortages in appliances and 87% of builders said they reported shortages in windows and doors according to the National Association of Home Buildings.

Why is this happening? Well, during the pandemic companies laid off employees to cut costs and companies had inventories that they thought would be enough based on the data that they had at that specific time. Then, new home sales absolutely surged, suppliers wiped out their inventories, and labor shortages continued despite supply chains revamping back up in 2021.

Conclusion: Building materials will continue to be a headwind and prices could continue to pressure builders. Manufacturers that we follow are still having shortages in raw materials/truck shortages/and issues with port backlogs.

Energy:

Energy prices in the United States have surged in 2021 and there are no signs of things slowing down anytime soon. How does energy prices impact the economy? Energy prices effect prices directly throughout the entire supply chain all the way from the initial input costs to the eventual transportation of those goods to the consumer. At the end of the day, these costs are eventually passed on to the consumer in the form of higher prices. Last year, gas prices in September were roughly $2.27 a gallon. Look forward to this September and prices are exactly $1 more per gallon sitting at $3.27, a 44% increase from last year.

Is an energy crisis looming? Possibly… Europe is currently dealing with their own energy crisis and looks to be getting worse by the minute. Right now, in Europe, heating your home costs 5x more this year than it did a year ago. Why is this happening? A couple of reasons. The world experienced a very cold winter last year which causing demand to surge leaving gas storage facilities depleted. Usually, these reserves are then restocked over the summer months but due to COVID many of these producers had to play significant catch up as demand soared. Europe is now hopeful that Russia can increase gas supplies for the upcoming winter months so the gas crunch could be alleviated. Governments are also pushing to cut global carbon emissions which is leading to the surge in natural gas prices as well. Unfortunately, this has had some negative repercussions in the short-term as coal demand is soaring to fill the gap in place of higher natural gas prices. U.S. power plants will burn 23% more coal this year than they did in 2020. While I think this is short-lived, it’s a reminder that moving away completely from fossil fuels is something that is quite frankly going to take some time to resolve.

At what point does it become an issue for consumers? Right now, energy costs as percentage of GDP are sitting at 5.2% according to Bernstein. If energy prices surge to a total of 7% of GDP, for a period longer than a year, than a recession could be possible. From the looks of it, energy prices are still within an acceptable range at the current time, but this is a critical aspect to the global economy and needs to be watched.

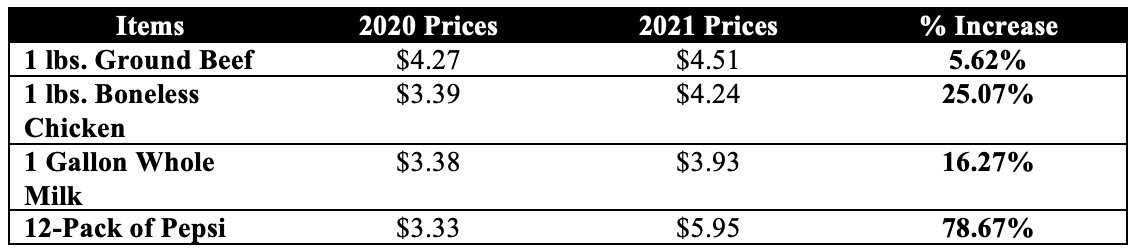

Food:

Now moving on to food costs in the United States, Americans have seen a meaningful uptick in prices over the last year. Households are now spending roughly $175 a month extra on food, housing, and gas. If we look at the chart below, there are some alarming price increases. Makes you wonder if you are willing to pay a 78% premium for that 12 pack of Pepsi the next time you head to the grocery store.

Source: Bloomberg

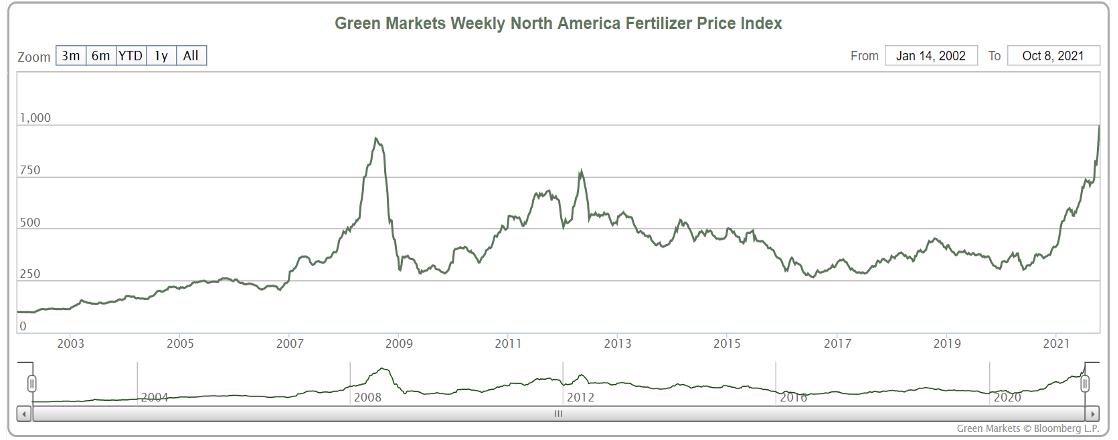

Another major issue hitting food prices is fertilizer costs. If we look at the Green Markets North America Fertilizer Price Index, this index gives a snapshot of where fertilizer prices are currently at.

This chart is going parabolic in recent months putting more pressure on companies around the globe who are being forced to raise prices across the board.

Source: Bloomberg

What is causing this? Natural gas prices. Natural Gas is the main ingredient when manufacturing nitrogen-based fertilizers which are used for corn and wheat. Natural gas is more than 70+% of the operating costs in the production of nitrogen. According to a Bloomberg Analyst (Alexis Maxwell), fertilizer costs could push up the cost of production by 16%.

Conclusion: Unfortunately, these surges in food prices may take much longer to correct themselves. We think it’s possible prices may rise even further in 2022.

Shipping/Trucking/Rail Costs:

Another issue over the last 6-12 months is the price of shipping containers. This has been one of the major influences on the higher amounts of inflation that Americans are experiencing. If we look at the chart below, shipping rates have more than quadrupled since June of 2020.

The port of Los Angeles, one of Americas largest ports, is operating 24/7 to hopefully relieve some of the backlog they’re experiencing. Trucking costs are up marginally since 2020, but rail rates have surged materially higher; up over 60+% since last summer. Truckers are in demand across the entire country and the lack of truckers are pushing companies to utilize the rail system to transport goods.

Autos:

Another area that has seen significant shortages is the auto market. If we look at the chart below, auto inventory levels have collapsed to their lowest levels in our dataset. As people pushed out of the cities due to the pandemic, cars were being bought at a record pace as mass transit was not being utilized during COVID outbreak.

Source: Bloomberg

How has inflation impacted the price of new cars? No secret here, prices of new cars have been moving materially higher from an average price of $35,000 in early 2020 to now $42,500, a 21% from a little over a year ago. This is the fastest pace of increases that I found on record for new vehicles in a very short period of time.

No inventories mean significantly higher prices for used cars as well. The Manheim US Used Vehicle Value Index has risen over 50+% in the last year or so due to overwhelming demand for cars. Do you have an extra car you’ve been thinking to sell? Now might be the right time as it’s never been a better time!

Source: Bloomberg

Conclusion: My best guess is as things improve and the virus becomes less impactful hopefully in the near term, people will start heading back to the cities again. This should bring some supply back on the market and will hopefully cool down the prices of used cars. As for new cars, unfortunately, I think with a global chip shortage and higher input costs across the board, I think new car prices will remain slightly more elevated than normal. Just to note, one car can have anywhere from 500-1,500 different types of chips on board depending on the make and model of the car. Next time you head to the dealership, be prepared to pay up and unfortunately, they have the upper hand when negotiating the price.

What should investors do in this environment?

Personally, I think investors should research assets such as Bitcoin, real estate, and gold. These assets could be the biggest beneficiaries of this global monetary experiment that is contributing to a sustained inflationary environment for the foreseeable future. Gold has not performed anywhere near as well as Bitcoin during this rapid rise in inflationary pressures. I know some of you may disagree about Bitcoin and consider it worthless, but one thing I learned is the Bitcoin community is very powerful and something special. It’s hard to call something worthless when at this point its trading at $63,000. Who knows what the future holds for Bitcoin, but at the present time, the “store of digital value” argument is alive and well.

While COVID is the main driver behind many of the issues we’re currently experiencing, I also still think major central banks around the world are backed into a corner. They say they have “tools”, but the tool they would turn to in a normal environment would be to hike interest rates. There is only one major problem. This time is different as global supply chains are a disaster and raising rates doesn’t solve shortages in all aspects of the economy.

So, the better question is why are they still using emergency measures when the economy seems to be holding its own? Simple. The Fed knows our fiscal deficits are nearing an unsustainable level and any increase in interest rates would lead to higher interest payments for the government. If the Fed is forced to hike interest rates quickly due to soaring inflation, it would be catastrophic for the United States and the global economy. Depending on how high interest rates go, the interest alone could be higher than 20+% of our total GDP each year just in interest payments. The U.S. has a major spending problem and it’s only going to get worse over the next 30 years. Below is an excellent chart depicting the treasury issuance vs. Fed purchases. While the Fed purchased the 2nd largest annual number of treasury/mortgage-backed securities, the issuance net of Fed Purchases in 2021 was a significant deficit relative to 2020 when the Fed was buying everything in sight.

Credit to Roberto Perli at Cornerstone Macro for the chart.

According to the CBO (Congressional Budget Office), the Federal Debt held by the public is projected to equal 202% of GDP by 2051.

Source: CBO

Will this lead to a future financial crisis? I don’t think in the near term, but the concerns longer-term have grown after the pandemic. I think investors are starting to become uneasy about the recent rise in inflation and investors seem to be cautious over the government’s fiscal position. It’s possible the U.S. at some point in the future will see a restructuring of its debt. I know that’s hard to believe, but this is on the table if there is not meaningful change with spending. Only fiscal responsibility is the right answer to solve the eventual currency/debt crisis in the future.

Can it be fixed? One solution is to dramatically raise taxes and slow down the amount of fiscal spending. The first part of the solution (raising taxes) is likely but slowing down the amount of spending will remain very difficult. I think higher taxes are on the way for the foreseeable future and the Fed will continue to monetize the uncontrollable spending by the government. This at some point will lead to a potential currency crisis as purchasing power will drop substantially and lead to higher amounts of inflation… Sounds like what’s happening right now….

The government should take advantage of these low interest rates while they can and issue 50 and 100-year bonds to finance the near-term spending packages. There is a tremendous amount of capital that is chasing yield from pensions, mutual funds, and institutional investors looking to park their money in a so called “safe asset”. The government won’t need to worry about refinancing debt at higher interest rates if rates go up in the future which seems to be extremely likely from these record low levels we have seen in the last few years.

Summary: I think a lot of people are suggesting we’re heading towards hyperinflation or stagflation. While it’s possible, I think we’re having a lot of these issues due to significant global demand for raw materials that are playing catch up from the COVID outbreak in 2019-2020. Demand remains robust and I don’t see any signs of letting up yet. This is a positive sign for the overall economy as supply chains start returning to full operation and things start to normalize back to pre-pandemic levels. I don’t think certain pockets of the economy will normalize anytime soon as these bottle necks will remain a challenge for the foreseeable future. Energy prices are a major factor, and this is one area that is a major cause for concern if prices accelerate meaningfully higher from here. Sustained inflation will at some point put a dent in the consumers pocket and the overall economy will slow down. At this point, the economy is booming and as long as inflation doesn’t move materially higher from here, I think the economy will continue to expand for the foreseeable future.

Thanks for reading and please subscribe to receive future updates. Please forward to anyone who you think can benefit from this information.

Cheers,

Korey Bauer

The publication of this newsletter falls outside of the scope of Korey Bauer’s (“Bauer”) employment with AXS Investments, LLC (“AXS”), and Bauer does not represent AXS in its publication. The views expressed in the newsletter solely represent the opinion of Bauer and do not reflect the views or opinions of AXS. Bauer’s opinions are subject to change and are not intended as a forecast or guarantee of future results, or investment advice. Stated information is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While Bauer believes the information to be accurate and reliable, he does not claim or have responsibility for its completeness, accuracy, or reliability. The newsletter is made available for informational and educational purposes only, and is not intended to be a substitute for professional investment advice tailored to your specific circumstances. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Bauer’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. These are Bauer’s views, and no company is responsible.

Exclusion of Liability: To the fullest extent allowed by law, neither AXS Investments, LLC nor Korey Bauer shall be liable for any direct, indirect, or consequential losses, loss of profits, damages, punitive damages or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this newsletter, which is provided as is and without warranties.

Charts/Sources from Bloomberg, CBO, Cornerstone Macro, J.D. Power)