Strength of U.S. Consumer

Strength of U.S. Consumer

What is the current outlook for U.S. Consumers?

I hope everyone is doing well and is staying healthy out there! Welcome new subscribers! Nothing that I say below is investment advice and the views below are subject to change at any time. These views are my views and not of any firm that I am associated with. Please read the disclosure at the end of this article for more information. Subscribe below!

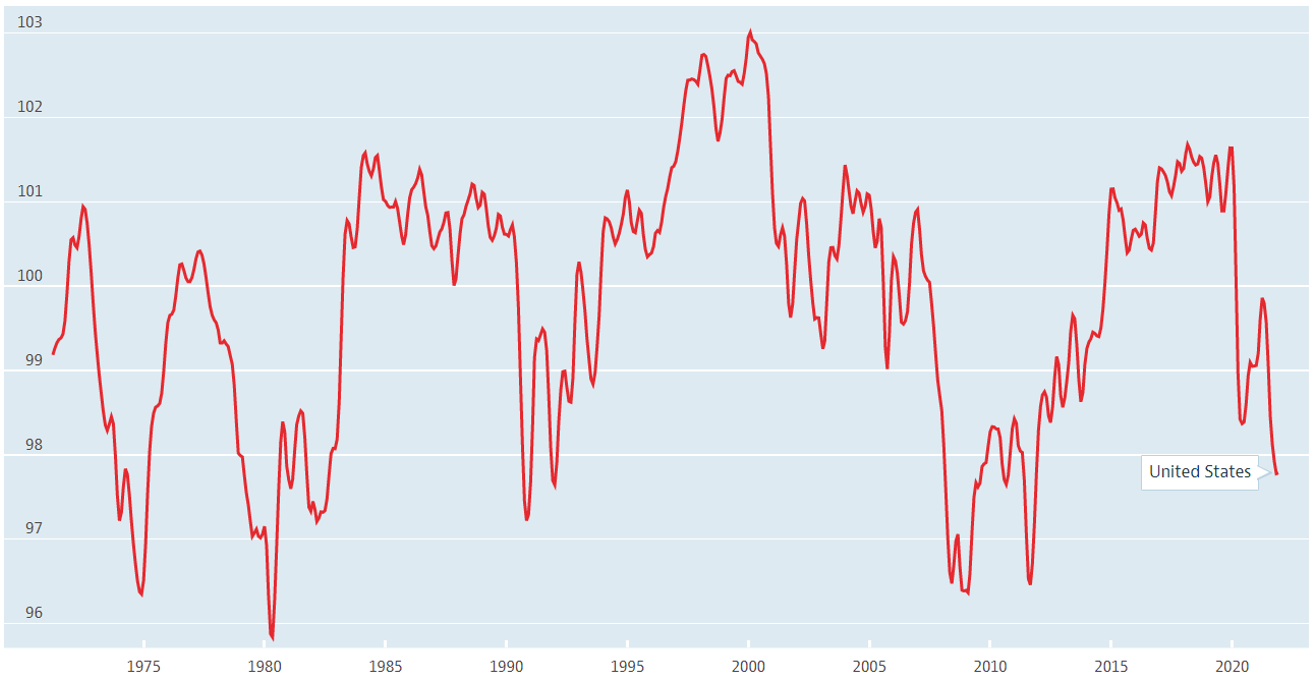

Today, we’re going to examine the U.S. consumer. If we look at the chart below, we can see that consumers are starting to really feel the heat from the inflationary pressures we discussed in our prior articles. The indicator depicts when above 100 a boost in consumer confidence towards the future economic situation. This leads to more spending in the economy over the course of the next 12 months. On the other hand, when below 100, consumers are pessimistic towards the future developments of the economy. Consumers tend to save in this environment and feel less confident to spend over the coming 12 months. Is this a bad sign for the economy? It seems that we may experience a slowdown in the near-term which seems to be reflective in the recent volatility we’re experiencing in the stock market. But, as we look forward, we believe COVID will have less impacts on supply chains and the economy as we move towards the spring/summer.

OECD (2022), Consumer confidence index (CCI) (indicator). doi: 10.1787/46434d78-en (Accessed on 19 January 2022)

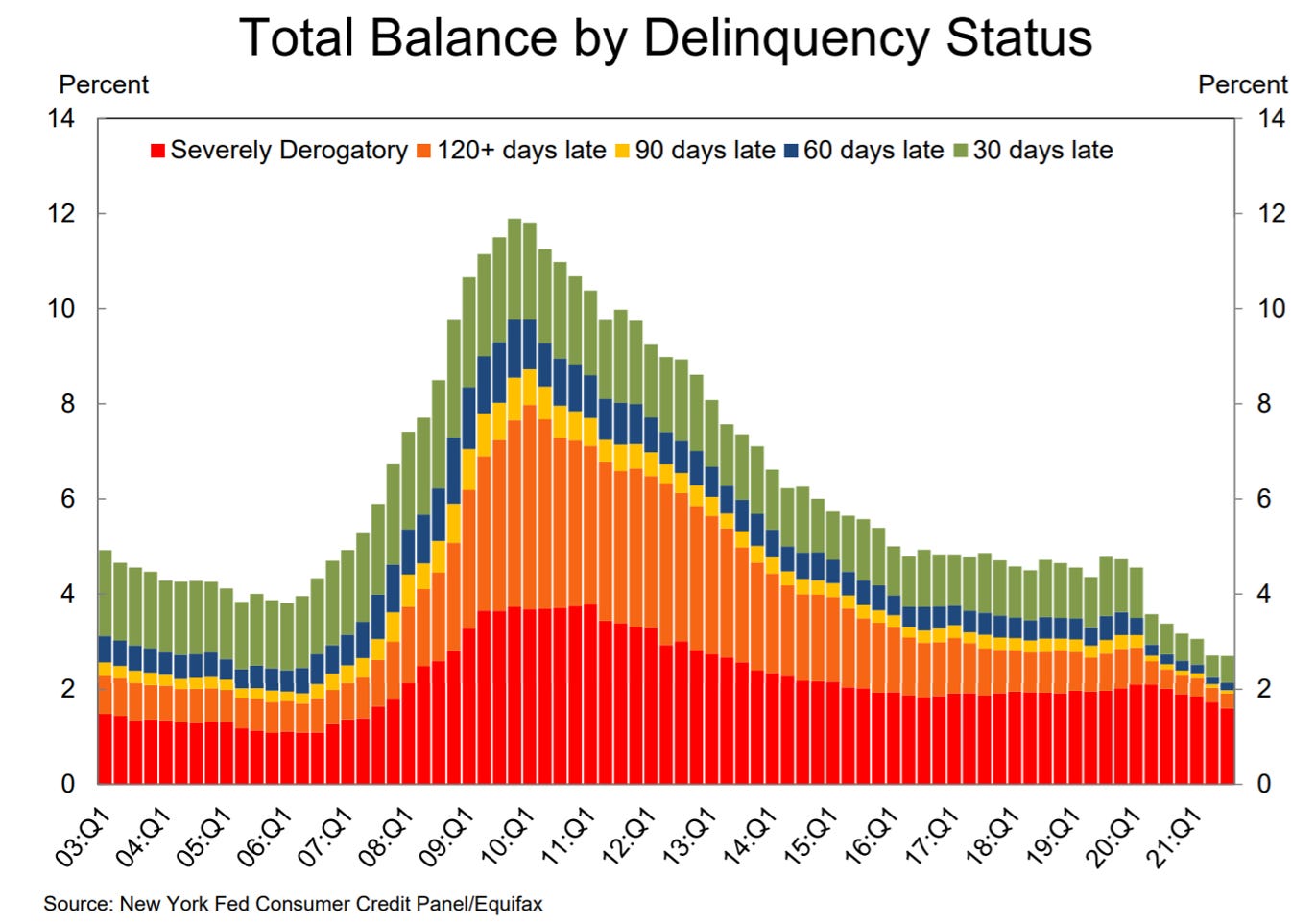

The bigger question as consumer confidence is falling, are consumer delinquencies ticking higher? It’s quite the opposite right now. Consumer balance sheets have strengthened considerably since the pandemic bump we saw in 2020.

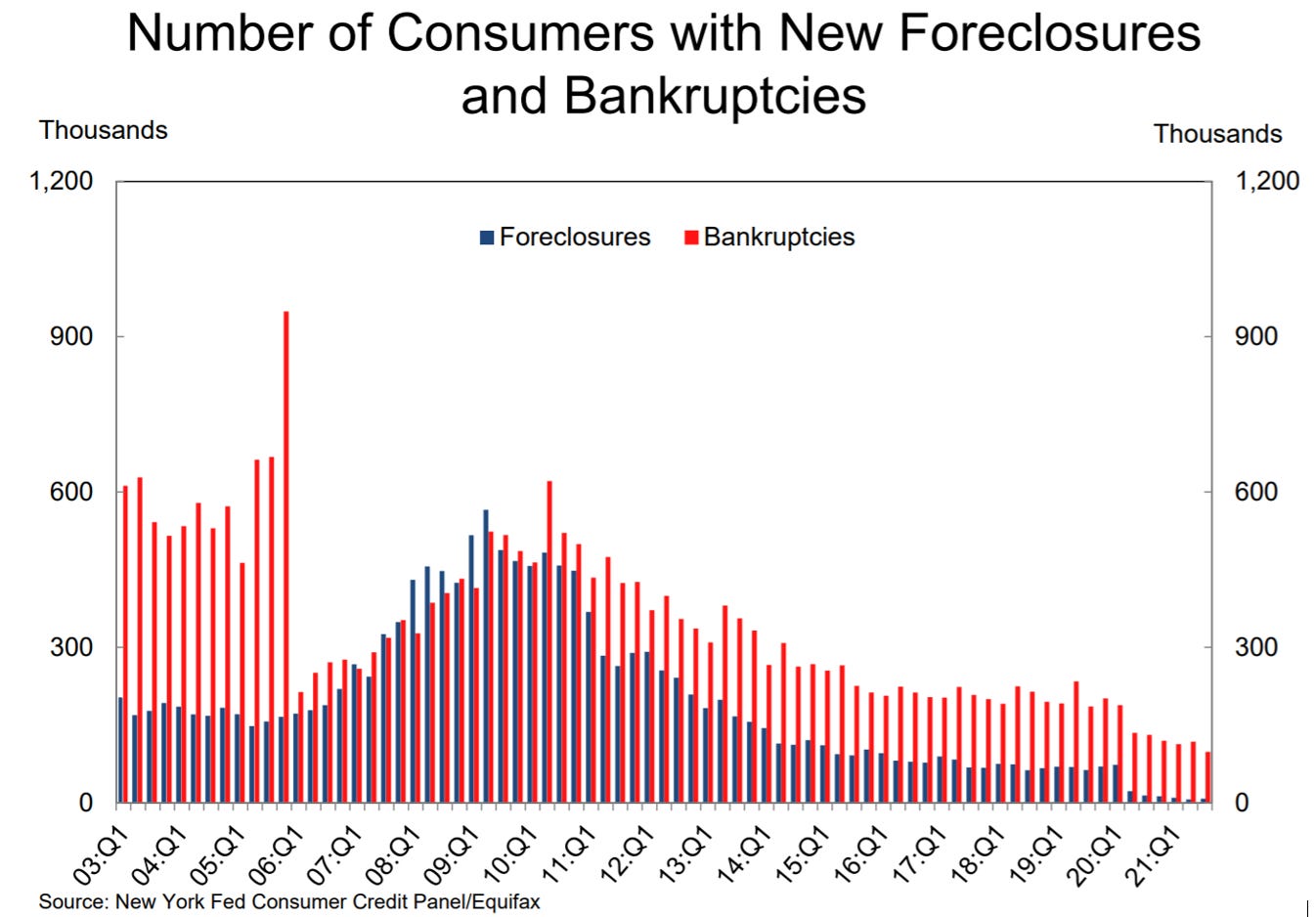

Let’s take it a step further and look at the number of consumers with new foreclosures and bankruptcies. You will notice the positive trend continues despite the high amounts of inflation we currently are experiencing.

What is one the main drivers of overall improvement? Well, if we look deeper student loan debt 90+ days delinquent has dropped sharply, thanks to the federal government’s role in delaying federal student loan repayments. The president recently extended this deadline back on December 22nd for an additional 90 days through May 1st, 2022. While this is helpful in the short-term there is still $1.6 trillion in student loan debt outstanding with the average amount owed being roughly $36,000.

Conclusion: While consumer confidence is waning and inflation is putting a dent in consumers’ pockets, consumers balance sheets remain strong. I am still in the camp that inflationary pressure should start to abate towards the end of 2022. The Fed will start to normalize rates this year with a few rate hikes that could cause a slight slowdown in activity, but I still believe the economy will remain strong and will continue to expand despite these near-term headwinds. Also, if risk assets decline significantly further, you can expect the Fed to reverse course and maintain simulative measures.

Thanks for reading and please subscribe to receive future updates. Please forward to anyone who you think can benefit from this information.

Cheers,

Korey Bauer

The publication of this newsletter falls outside of the scope of Korey Bauer’s (“Bauer”) employment with AXS Investments, LLC (“AXS”), and Bauer does not represent AXS in its publication. The views expressed in the newsletter solely represent the opinion of Bauer and do not reflect the views or opinions of AXS. Bauer’s opinions are subject to change and are not intended as a forecast or guarantee of future results, or investment advice. Stated information is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While Bauer believes the information to be accurate and reliable, he does not claim or have responsibility for its completeness, accuracy, or reliability. The newsletter is made available for informational and educational purposes only and is not intended to be a substitute for professional investment advice tailored to your specific circumstances. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Bauer’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. These are Bauer’s views, and no company is responsible.

Exclusion of Liability: To the fullest extent allowed by law, neither AXS Investments, LLC nor Korey Bauer shall be liable for any direct, indirect, or consequential losses, loss of profits, damages, punitive damages or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this newsletter, which is provided as is and without warranties.