2023 Outlook... Will the downturn continue?

2023 Outlook... Will the downturn continue?

I hope everyone is doing well! Welcome to all my new subscribers!

Nothing that I say below is investment advice and the views below are subject to change at any time. These views are my views and not of any firm that I am associated with. Please read the disclosure at the end of this article for more information. Subscribe below!

Hey everyone! It’s been a brutal year for global markets, but the big question is, will it continue in 2023? Unfortunately, there are so many headwinds that I personally believe things will remain very rocky for the foreseeable future. Before we jump into the 2023 outlook, let’s do a quick recap of 2022.

2022 was the largest loss in history for the global bond and stock market combined. Over $35 Trillion was wiped-out!

Source: Bloomberg

The 60/40 portfolio had its worst annual performance in the past 100 years!

Source: BofA

So, are we in recession? The probability of a US Recession predicted by the Treasury spread (10 year bond rate – 3-month bill rate) is at the highest levels during the COVID crisis and 2008 recession. One can see most times we breach the 0.4 (40%) level and recession usually follows. As of November, the probability of recession is at 38.05%.

Source: NY FED

A big concern of mine is wages matching the pace of inflation. Unfortunately, prices have increased faster than wages for a record 20 consecutive months! Consumers are getting crushed with price hikes and the economy is slowing.

Bloomberg/Zerohedge

One of the biggest areas of concern is the auto market. I fear for the worst in 2023 if interest rates remain elevated throughout the year. Here are some things to consider:

The cost of a new car is up 7.2% over the last year as auto makers are forced to raise prices due to higher labor and input costs for their vehicles. The Manheim used vehicle index is still at extreme levels despite the recent weakness in used car prices. Some dealers bought cars at inflated values and now will be left holding the bag as consumers become more cost conscious.

Source: Manheim

Consumers who are buying new vehicles with trade-ins are seeing the biggest average negative equity. (The loan is worth more than the vehicle)

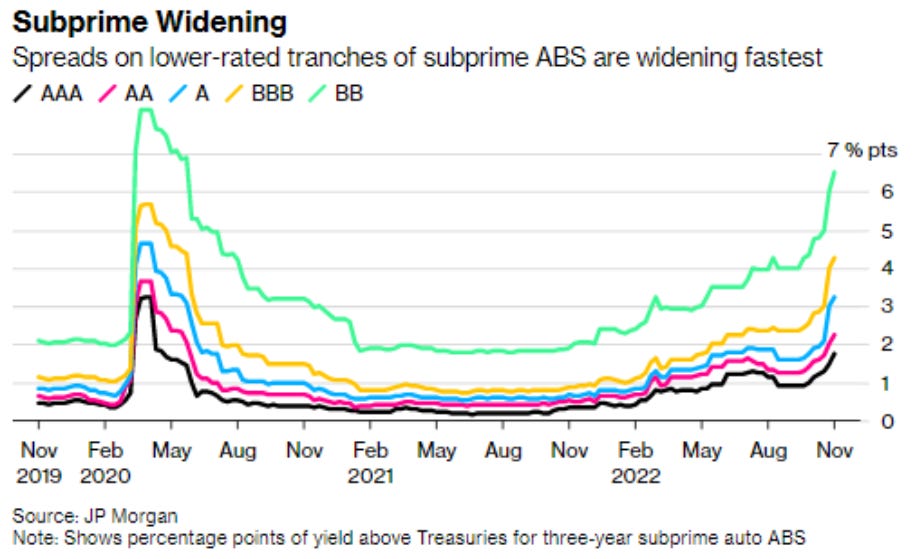

Auto subprime is also widening. More signs of stress in the auto market. Expect a flood of inventory if the economic decline deepens.

Source: JP Morgan

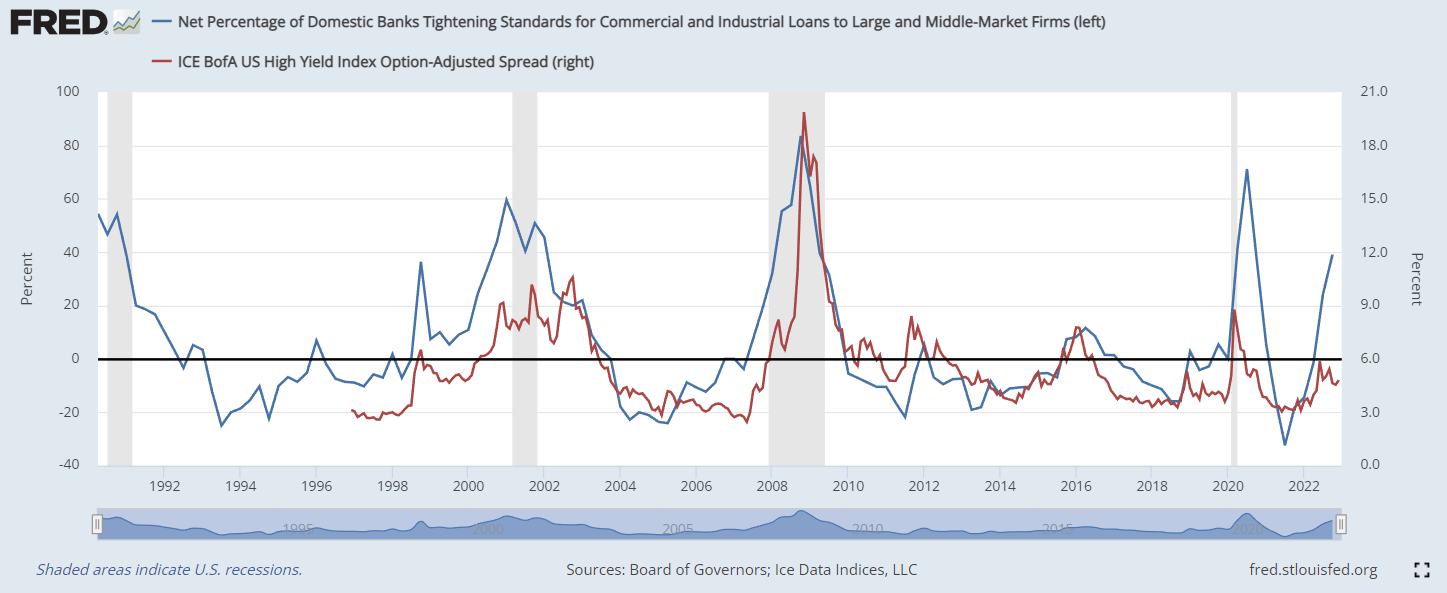

Another area of concern is the rapid tightening of credit standards for C&I Loans. The chart below depicts the blue line which shows the net percentage of banks tightening credit standards for loans. When the blue line is higher, banks start to tighten credit conditions, which is usually a time we see credit markets start to weaken as well. There seems to be a big divergence between lending standards and credit spreads which in my opinion won’t last. Either banks are being overly conservative, or the economy is about to bounce back.

Also, the personal savings rate is crashing and burning. The personal savings rate was at 2.3% as of October, which is down from 7.3% a year ago. The personal savings rate measures how much Americans’ after-tax income is left after spending money on food, bills, and other expenses. In conclusion, Americans are only saving $2.30 on every $100 they earn. This is a major warning sign for the economy.

Conclusion – Unfortunately, I think we are already in a recession. How deep it gets is anyone guess. One thing is for sure, any further disruptions with supply chains or further geo-political issues could easily tip the global economy over.

Now let’s discuss the housing market.

The U.S. housing market over the last 12 months are starting to see some cracks as well. I don’t think we’ll see a repeat of 2008, but prices are extremely inflated due to the lack of inventory and surge in inflationary pressures. The average price of a new home in the U.S. is $471,200 as of November 2022.

But, the good news is that it seems housing prices have peaked temporarily as consumers are on a bit of a buying strike with higher interest rates.

As I mentioned above, I don’t think this will be another 2008 as most mortgage originations have 760 or higher credit scores. Back in 2008 this was less than 1/3 of all originations.

Existing home sales in the U.S. are crashing (down 35.4% Year over Year) as the steep rise in interest rates caused buyers to step away near record high home prices.

Will inventory problems be solved? If we look at the chart below, there has been an absolute explosion in new multi-family homes being built, which is the highest it has been since the 1970’s! I fear this might be the place we are seeing the excess froth relative to single family constructions, which I think is still underbuilt.

Now on to inflation - is the inflation shock over? I think so. Here’s a few reason’s why.

First let’s look at oil prices. Oil prices are collapsing, which is major tailwind for the U.S. consumer/businesses.

Second, natural gas prices are collapsing as well. Thankfully, for the global economy, the winter has been mild so far, except for the recent artic blast we experienced in the U.S.

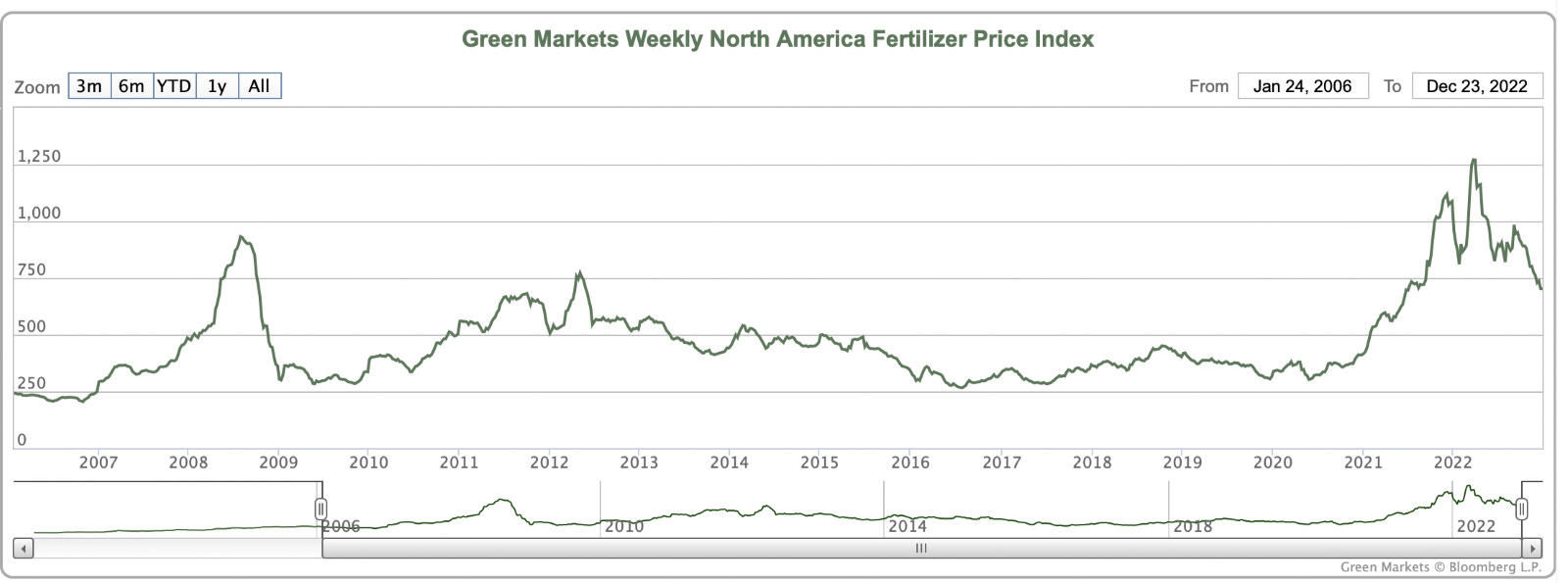

Food prices, which were one of my biggest concerns in 2022, unfortunately played out but I think as we move to 2023, consumers will get some relief as fertilizer prices are well off their all-time highs.

Can anyone say egg shortage? In California, a dozen eggs is $7.37!

I think 2023 is going to be a volatile year for the global equity markets. I expect at some point this year equity markets will have a sharp drop which will be quickly recovered like we have seen in recent years. The federal reserve is clearly overshooting with the speed of rate increases which will lead to them cutting by the end of this year or early next year. Stay safe out there and we will be hopefully sending out weekly technical updates on the market.

Lastly, I wanted to share something going into the new year. Microsoft did a study on 14 people across two days of meetings. Summary: back to back meetings promote stress. Short breaks in between meetings allowed the brain to rest and never have any stress buildup. Pace yourself in 2023!

Source: @sahilbloom/Microsoft

Thanks for reading! Happy New Year!

Cheers,

Korey

The publication of this newsletter falls outside of the scope of Korey Bauer’s (“Bauer”) employment with MFAC, and Bauer does not represent MFAC in its publication. The views expressed in the newsletter solely represent the opinion of Bauer and do not reflect the views or opinions of MFAC. Bauer’s opinions are subject to change and are not intended as a forecast or guarantee of future results, or investment advice. Stated information is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While Bauer believes the information to be accurate and reliable, he does not claim or have responsibility for its completeness, accuracy, or reliability. The newsletter is made available for informational and educational purposes only and is not intended to be a substitute for professional investment advice tailored to your specific circumstances. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Bauer’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions which may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. These are Bauer’s views, and no company is responsible.

Exclusion of Liability: To the fullest extent allowed by law, neither MFAC nor Korey Bauer shall be liable for any direct, indirect, or consequential losses, loss of profits, damages, punitive damages or costs or expenses incurred or suffered by you arising out or in connection with the access to, use of, or reliance on any information contained in this newsletter, which is provided as is and without warranties.